$812 a Month. That’s What Americans Are Paying for a New Car in 2026 — And It’s Getting Worse : Eight hundred and twelve dollars. Every single month. Just for the car.

That’s the average new car payment in America right now — and according to JD Power’s latest April 2026 forecast, it’s up 3.1% from last year. Not because cars got more expensive. Not because interest rates jumped. But because of something way more dangerous: negative equity is quietly swallowing American car buyers whole.

And new car sales just dropped 7.3% in April. So yeah — the market is telling us something.

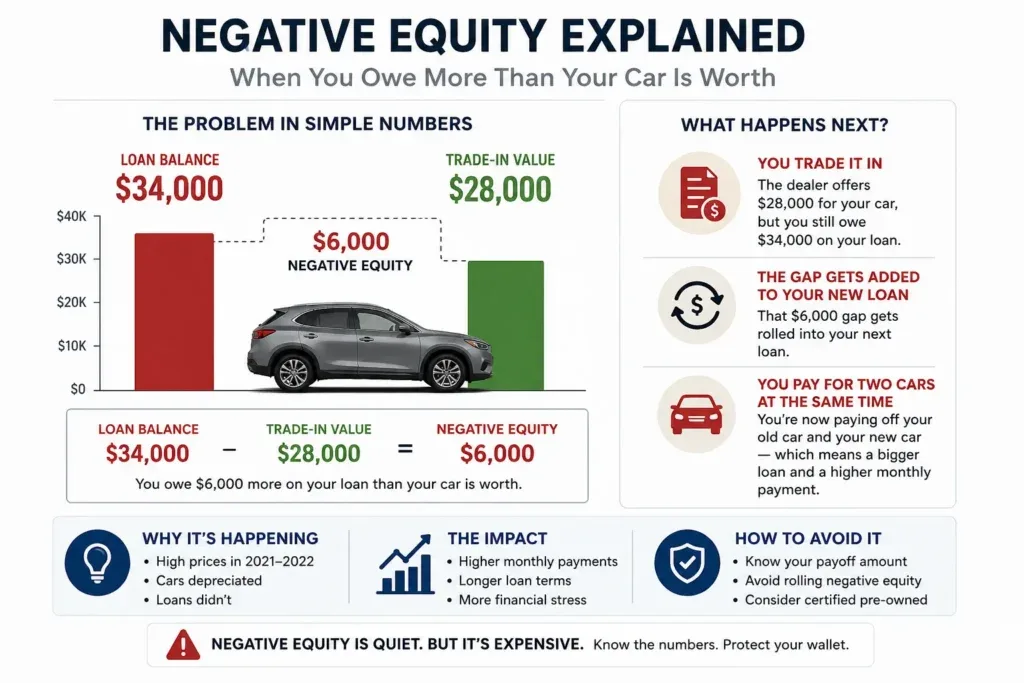

Wait, What Even Is Negative Equity?

Simple. You bought a car two years ago for $45,000. You financed it, made payments, and now you want to trade it in. Problem? The dealer offers you $28,000 — but you still owe $34,000 on the loan.

That $6,000 gap? That’s negative equity. And dealers roll it into your next loan. So now you’re paying off your old car AND your new car at the same time — and wondering why your payment feels like a second rent.

This is happening everywhere right now. The pandemic-era car buying frenzy of 2021-2022 — when people paid $5,000 over sticker for a basic Camry — is now coming back to bite those exact same buyers. Those cars depreciated. The loans didn’t.

The 7.3% Sales Drop — But Don’t Panic Yet

Here’s the thing about the April sales drop: it’s not as scary as it sounds.

Last April, tariff panic sent 53,000 extra buyers rushing to dealerships ahead of expected price hikes. That artificial spike made April 2025 look huge. Compare against that and of course 2026 looks bad.

The real underlying sales pace — the SAAR — is tracking around 16 million units. That’s actually close to normal. Not great, not terrible.

But the affordability squeeze is real. Compact SUVs — the bread and butter of the American auto market — are actually selling below the overall industry average right now. When the people who would normally buy a $35,000 Kia Sportage can’t afford it, that’s a problem that doesn’t fix itself quickly.

also read https://driveglobalnews.in/u-s-news-just-named-the-best-hybrids-and-evs/

So What Should You Actually Do?

If you’re in the market for a new car right now, three things matter more than anything else:

Know your payoff amount before you set foot in a dealership. Call your lender, get the 10-day payoff figure, write it down. If the trade-in offer doesn’t cover it — do not roll that gap into a new loan. Walk away if you have to.

Seriously consider certified pre-owned. A 2-year-old hybrid with 20,000 miles doesn’t have the tariff premium baked in, doesn’t have the negative equity issue, and comes with most of the factory warranty intact. Right now, that’s genuinely smart money.

Don’t buy above your means just because rates look okay. A 6.5% rate on a $50,000 vehicle for 72 months is $852 a month. Add insurance, gas, and maintenance — you’re at $1,200 a month for a car. For most families, that’s simply too much.

The $812 average payment isn’t just a number. It’s a warning sign. The buyers who ignore it are the ones who’ll be rolling $10,000 of negative equity into their next car two years from now.