Does Your Credit Score Affect Car Insurance in 2026 : Imagine this.

Two drivers live in the same neighb orhood.

They drive similar vehicles.

They have clean driving records.

No accidents.

No speeding tickets.

No insurance claims.

Yet one driver pays hundreds of dollars more every year for the exact same coverage.

Why?

Because of a number that has nothing to do with driving.

Their credit score.

For many Americans, discovering this feels confusing.

For some, it feels unfair.

But in 2026, the reality is simple.

In many states, your credit score can absolutely affect what you pay for car insurance.

Just not everywhere.

Why Insurance Companies Look at Credit

Insurance companies don’t typically use your traditional credit score directly.

Instead, many insurers rely on something called a credit-based insurance score.

It’s designed to help predict the likelihood of future claims.

Insurers argue that years of data show a connection between credit history and claim frequency.

In other words, they believe drivers with lower credit scores are statistically more likely to file claims.

Consumer advocates disagree.

They argue that financial history doesn’t necessarily reflect driving ability.

Both sides continue debating the issue.

But for now, credit remains part of the pricing formula for many insurers.

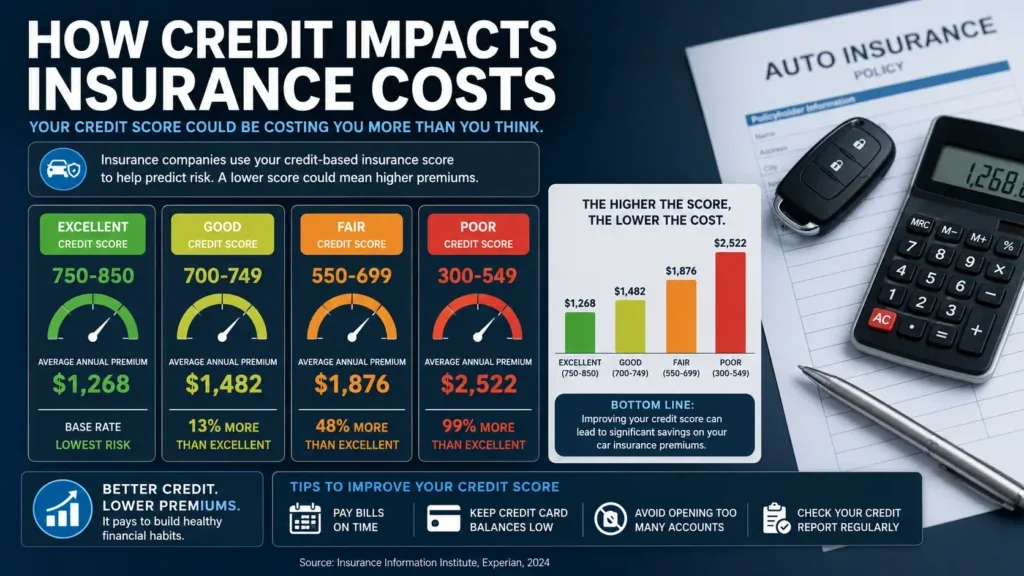

How Much Can Credit Affect Your Premium?

The answer varies.

Your state matters.

Your insurance company matters.

Your driving record matters.

But here’s the important part.

The impact can be significant.

Drivers with poor credit often pay 20% to 80% more than drivers with excellent credit for similar coverage.

In some cases, the difference can be even larger.

Over several years, that gap can add up to thousands of dollars.

That’s why understanding this issue matters.

Even if you have a perfect driving history.

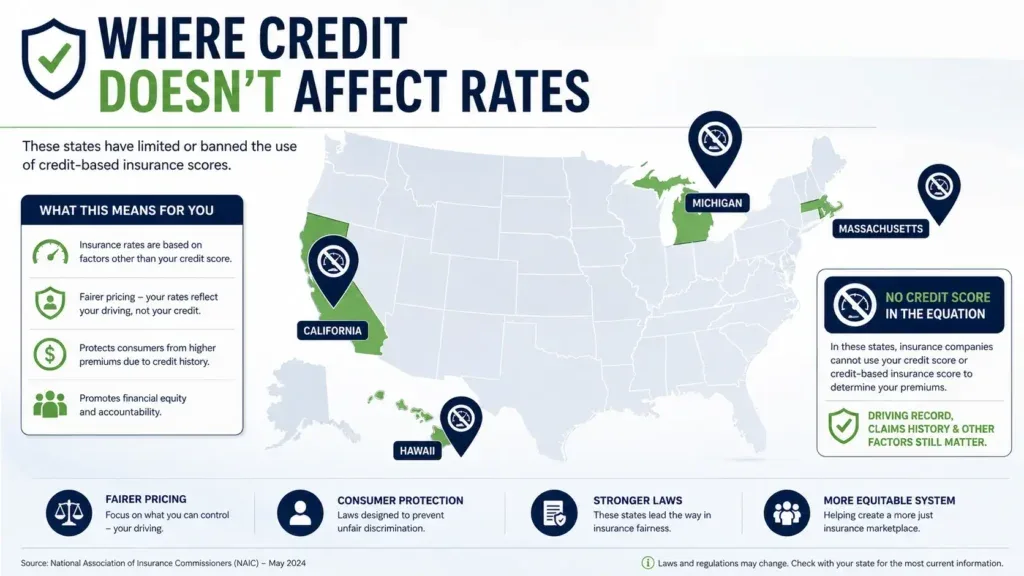

Not Every State Allows It

This is where things become more complicated.

Insurance rules differ across the country.

Several states restrict or prohibit insurers from using credit information when setting premiums.

These include:

- California

- Hawaii

- Massachusetts

- Michigan

If you live in one of these states, your credit score generally won’t affect your auto insurance rates.

For everyone else, it probably will.

That’s why two drivers with identical profiles can receive very different quotes depending on where they live.

Why This Matters More in 2026

Insurance costs are rising.

Repair costs continue increasing.

Modern vehicles include expensive sensors, cameras, and advanced safety systems.

Medical costs remain high.

Extreme weather events create more claims.

As overall premiums climb, the effect of credit becomes more noticeable.

A higher percentage increase on an already expensive policy hurts even more.

Also Read:

https://driveglobalnews.in/car-insurance-for-bad-credit-2026-how-much-more-are-you-paying/ – How much extra drivers with poor credit could pay this year.

Can You Improve Your Insurance Rate?

Yes.

But it takes time.

Improving your credit profile may help reduce premiums over the long term.

Pay bills on time.

Reduce outstanding balances.

Review your credit reports for errors.

Avoid opening unnecessary accounts.

At the same time, don’t overlook other opportunities to save.

Shop around regularly.

Bundle policies.

Ask about discounts.

Increase your deductible if it makes sense financially.

Different insurers weigh credit differently.

That’s important.

One company might offer significantly better rates than another.

Your Driving Record Still Matters Most

Credit is only one part of the equation.

Insurance companies also consider:

- Driving history

- Age and experience

- Vehicle type

- Annual mileage

- Location

- Coverage levels

A strong credit score won’t erase multiple speeding tickets.

And poor credit doesn’t automatically guarantee sky-high premiums.

Insurance pricing is based on the entire picture.

Not just one number.

Also Read:

https://driveglobalnews.in/5-cars-with-the-cheapest-insurance-for-families-in-2026/ – Family vehicles that can help keep insurance costs under control.

The Bigger Debate Isn’t Going Away

Should insurers use credit information at all?

It’s a question that divides consumers, regulators, and insurance companies.

Some believe insurance pricing should focus solely on driving behavior.

Others argue insurers should use any information that helps predict risk accurately.

That conversation will continue.

But while the debate plays out, drivers still have to navigate the system that exists today.

The Honest Answer

Many people assume car insurance is based entirely on how they drive.

In reality, it’s based on how insurers evaluate risk.

And in much of America, your financial history is part of that calculation.

You don’t have to agree with it.

But you should understand it.

Because knowledge saves money.

The next time your insurance renewal arrives and the premium feels higher than expected, don’t just look at your driving record.

Look at the bigger picture.

Because sometimes the factor affecting your insurance bill isn’t sitting in your driveway.

It’s sitting quietly inside your credit report.