Buying your first car is exciting — but the insurance bill can be a rude shock. In 2026, first-time buyers are paying some of the highest rates ever. Here’s how to not overpay from day one.

Why First-Time Buyers Pay So Much

Insurance companies see new drivers as high risk. No driving history means they don’t know how safe you are. Add in young age (if applicable) and expensive new cars, and premiums can easily cross $2,000–$4,000 per year for full coverage.

Smart Steps to Get Lower Rates as a First-Time Buyer

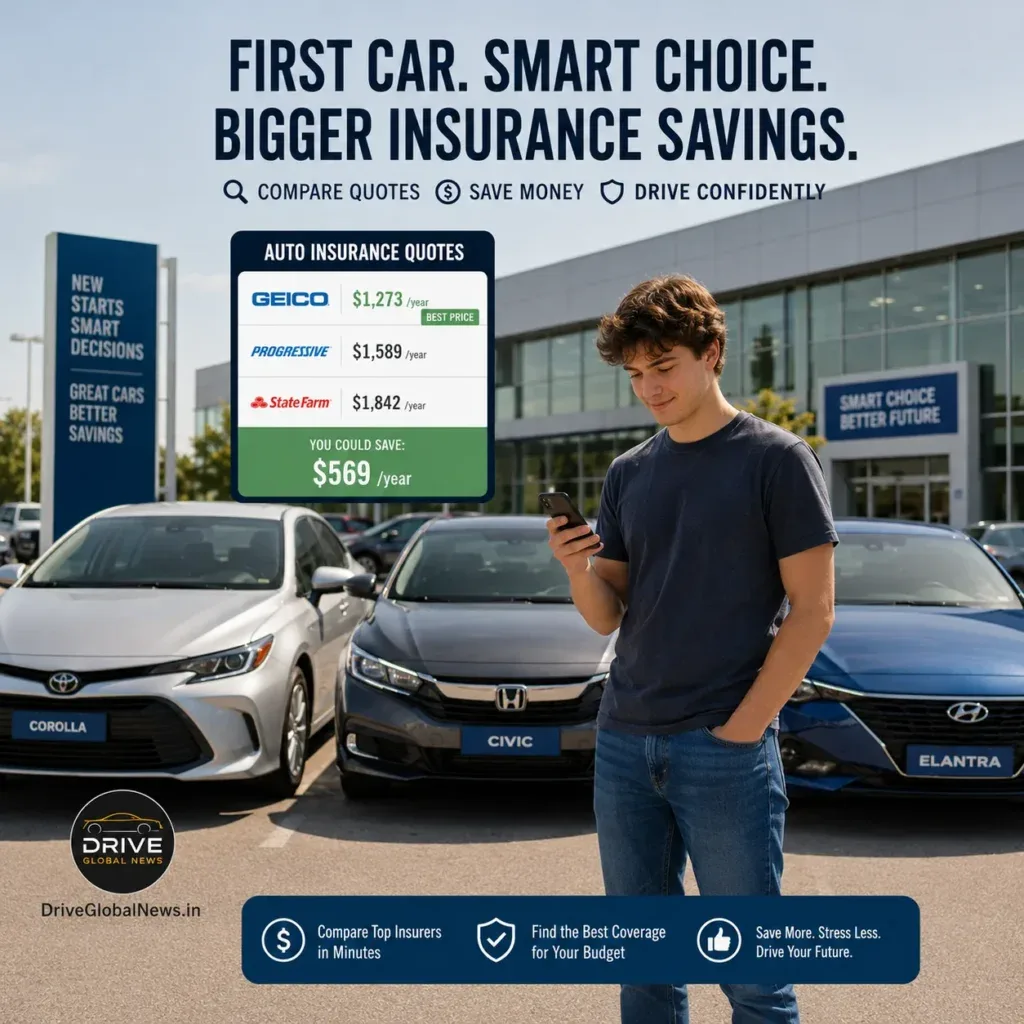

- Start With the Right Car Choose a vehicle with good safety ratings and low repair costs. Cars like Toyota Corolla, Honda Civic, and Hyundai Elantra are much cheaper to insure than sports cars or luxury models.

- Compare Multiple Quotes Never accept the first offer. Get quotes from at least 4-5 companies. Rates can vary by hundreds or even thousands of dollars for the same car.

- Consider Your Parents’ Insurance If you’re under 25, staying on your parents’ policy is often much cheaper than getting your own. Many insurers offer good discounts for this.

- Take a Defensive Driving Course Many insurance companies give discounts for completing an approved defensive driving course.

- Choose Higher Deductibles If you can afford to pay more out of pocket in case of a claim, raising your deductible can significantly lower monthly premiums.

- Bundle and Ask for Discounts Bundle auto with renters or home insurance. Ask about good student discounts, telematics programs (safe driving apps), and anti-theft discounts.

What Coverage Do You Actually Need?

As a first-time buyer, start with state minimum liability coverage if your budget is tight. But full coverage (including collision and comprehensive) is strongly recommended if you financed the car.

Realistic Expectations in 2026

Be prepared for higher rates in your first 2-3 years. As you build a clean driving record, your premiums will drop significantly every year. Many drivers see big savings after age 25 or after 3 years of claim-free driving.

The Bottom Line

Don’t overpay for car insurance just because you’re a first-time buyer. Shop around, choose an insurance-friendly car, and take advantage of every possible discount. The effort you put in now will save you thousands of dollars over the next few years.

If you recently had (or are worried about) an accident, read our detailed guide on car insurance after an accident in 2026. And if you’re looking for more affordable options, check our article on best hybrid cars under $30,000.

What was your experience getting insurance for your first car? Share your tips or struggles in the comments below — it will help other first-time buyers.