Nobody warns you about this before you get your license.

The car itself? Everyone talks about that. But the insurance bill that arrives a few weeks later — that’s the number that genuinely shocks new drivers and their parents.

A 16-year-old added to their parents’ policy costs an average of $2,100-$3,500 more per year in additional premium. An 18-year-old on their own policy pays an average of $4,500-$6,000 per year for full coverage. In high-cost states like New York, Louisiana, and Florida — those numbers climb past $6,000 and approach $8,000 for some profiles.

Here’s why it’s so expensive, which companies charge the least, and what actually works to bring the number down.

also read : https://driveglobalnews.in/cheapest-car-insurance-companies-in-2026/

Why New Driver Insurance Is So Expensive — The Honest Explanation

Insurance companies price risk. Young drivers are statistically the highest-risk demographic on American roads — by a significant margin.

The data is stark. Drivers aged 16-19 are nearly three times more likely to be in a fatal crash per mile driven than drivers aged 20 and older, according to NHTSA’s most recent figures. Teen drivers are more likely to speed, less likely to wear seatbelts, more likely to be distracted by phones, and less experienced at reading developing traffic situations.

Insurers aren’t being unfair. They’re being actuarial. The claims they pay out on 16-24 year old policyholders are genuinely higher than on middle-aged drivers with clean records. The premium reflects that reality.

The good news: that reality changes every year. Most insurers see meaningful rate reductions at age 21, again at 25, and again when a driver accumulates three years of clean driving history. The expensive years are genuinely temporary.

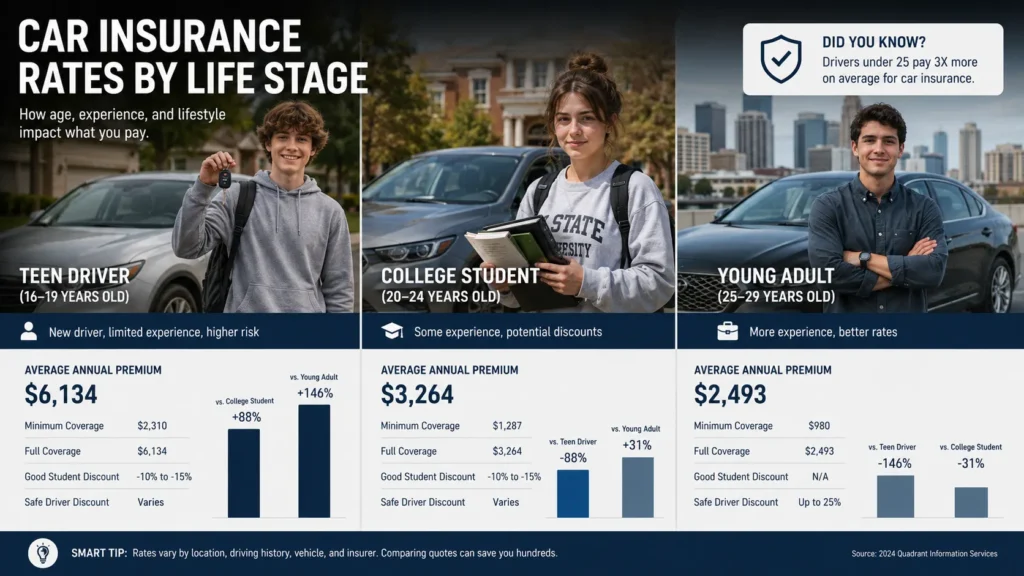

Real Rates by Age — May 2026

These are NerdWallet’s monthly averages for full coverage as of May 2026:

Age 16 (added to parent policy): Progressive: approximately $289/month additional ($3,468/year) State Farm: approximately $254/month additional ($3,048/year) GEICO: approximately $276/month additional ($3,312/year)

Age 18 (own policy, full coverage): Progressive: approximately $375/month ($4,500/year) Travelers: approximately $347/month ($4,164/year) GEICO: approximately $390/month ($4,680/year)

Age 21 (own policy, full coverage): Progressive: approximately $218/month ($2,616/year) Travelers: approximately $201/month ($2,412/year)

The drop from 18 to 21 is substantial — roughly $150-$175 per month less, just from aging three years with a clean record.

Age 25 (own policy, full coverage): National average drops to approximately $175-$195/month — very close to the standard adult rate.

The insurance expensive years run roughly from 16 to 24. After that, for drivers who maintain clean records, rates normalize to something manageable.

also read : https://driveglobalnews.in/ev-insurance-vs-gas-car-insurance-in-2026-which/

Which Companies Are Actually Cheapest for New Drivers

Progressive — best overall for young drivers

Progressive has consistently offered the most competitive rates for under-25 drivers among major national carriers. Their Snapshot telematics program is particularly valuable for young drivers: it tracks your driving via smartphone app and offers discounts of up to 30% for safe behavior. A young driver who genuinely drives carefully — no hard braking, no speeding, no late-night driving — can save $1,000-$1,800 per year through Snapshot compared to a standard Progressive rate.

State Farm — best for students with good grades

State Farm offers a Good Student Discount worth up to 25% off for students maintaining a B average or better. For a college student paying $4,500 per year baseline, that’s $1,125 in annual savings. The discount applies through age 25 for full-time students. Combined with State Farm’s generally competitive young driver base rates — particularly for drivers being added to a parent’s existing policy — this is often the cheapest option for students.

USAA — best for military families, unbeatable

If you or a parent have served in the US military, USAA’s young driver rates are the lowest available nationally — often 15-25% below the next cheapest option. A 20-year-old military dependent on a USAA policy pays dramatically less than the same driver on any other carrier. If you qualify, there’s no decision to make.

Travelers — best for new drivers who want straightforward coverage

Travelers doesn’t have the flashiest telematics program or the most prominent student discounts, but their base rates for young adults aged 21-25 are consistently among the three lowest of any major carrier. For a 22-year-old who has aged off their parents’ policy and wants reliable coverage at a competitive price — Travelers is often the answer.

5 Moves That Actually Lower New Driver Insurance Bills

Stay on your parents’ policy as long as legally possible. In most states, you can remain on your parents’ auto insurance policy as long as you live at their address or are a dependent. The additional premium for a teen on an existing policy is significantly lower than a standalone young adult policy. When you move out or buy a car in your own name — that’s when your rate jumps to the standalone young driver rate.

Choose the car carefully. The vehicle you drive matters enormously to your insurance rate. A 2022 Honda Civic costs dramatically less to insure than a 2022 BMW 3 Series for a young driver. A used, lower-horsepower vehicle with good safety ratings is the cheapest profile. Sports cars, luxury vehicles, and high-horsepower vehicles all carry significant insurance premiums — especially for young drivers who statistically make more claims in higher-performance vehicles.

Take a defensive driving course. Most states and most insurers offer a discount of 5-15% for completing an approved defensive driving course. At $4,500 per year baseline, a 10% discount saves $450 annually. The course costs $30-$75. The math works every time.

Use telematics programs. Progressive Snapshot, State Farm Drive Safe & Save, and Allstate Drivewise all track your actual driving behavior. Safe driving — meaning no hard braking, reasonable speeds, minimal late-night driving — earns discounts that can reach 30% on Progressive specifically. For a genuinely careful young driver, this is the single highest-value discount available.

Maintain a clean record obsessively. One at-fault accident adds 30-40% to an already expensive young driver premium. At $4,500 baseline, one accident adds $1,350-$1,800 to your annual bill — and follows you for three years. The financial cost of a single at-fault claim for a young driver is approximately $4,500-$5,400 in additional premiums over three years. That context makes careful driving a financial decision, not just a safety one.

The Bottom Line for New Drivers in 2026

Car insurance as a new driver is expensive. It’s not a mystery and it’s not random — it reflects real statistical risk that insurers price accurately.

The moves that work: stay on your parents’ policy, choose a boring car, drive carefully, use telematics, maintain good grades. None of these are complicated. All of them compound over time into meaningfully lower rates.

By 25 — assuming a clean record — you’re paying what everyone else pays. The expensive years are finite. Knowing that doesn’t make the bill less painful, but it makes it less demoralizing.