Car Insurance for Bad Credit in 2026 : A driver with a perfect driving record walks into an insurance company and gets a quote.

No accidents.

No speeding tickets.

No claims.

Then another driver with the exact same vehicle, the same age, and the same driving history requests a quote.

The only difference?

Their credit score.

One driver pays hundreds of dollars more every year.

Sometimes thousands.

If that sounds unfair, you’re not alone.

For millions of Americans, car insurance pricing remains one of the most confusing parts of vehicle ownership.

Most people understand why a speeding ticket increases premiums.

But credit scores?

That surprises people.

And in 2026, it continues affecting insurance costs across much of the country.

Why Insurance Companies Care About Credit

This is usually the first question drivers ask.

What does a credit score have to do with driving?

According to insurers, quite a bit.

Insurance companies often use something called a credit-based insurance score.

It’s not exactly the same as your traditional credit score.

But it’s closely related.

Insurers argue that drivers with lower credit scores statistically file more claims and generate higher costs.

Consumer advocates disagree with the practice, arguing that financial history doesn’t necessarily predict driving behavior.

Regardless of where you stand, the reality remains the same.

In many states, insurers can legally consider credit information when calculating premiums.

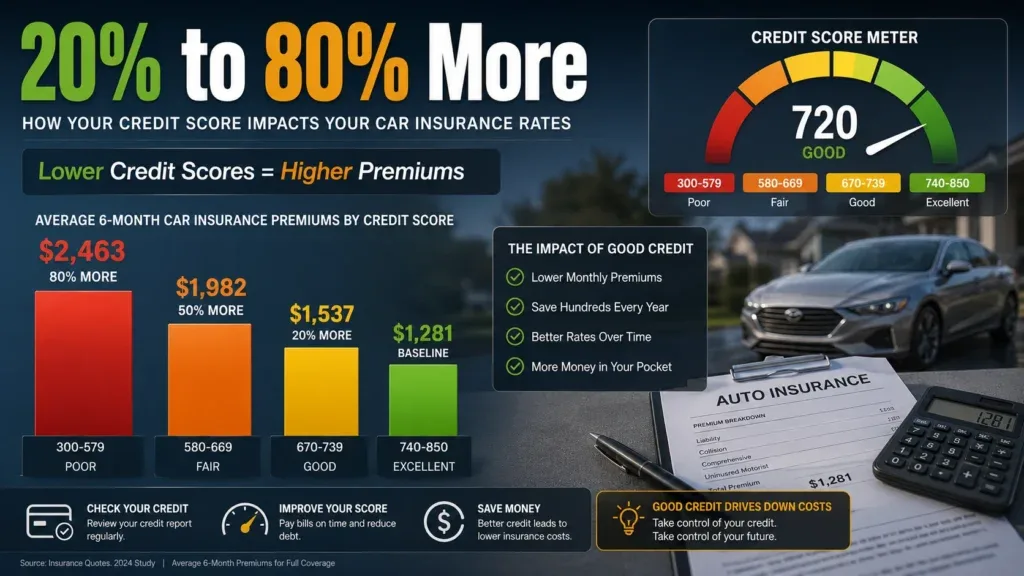

How Much More Could You Pay?

The answer depends on several factors.

Your state.

Your insurer.

Your age.

Your driving history.

Your vehicle.

But here’s the important part.

The difference can be significant.

Drivers with poor credit often pay 20 percent to 80 percent more for identical coverage compared with drivers who have excellent credit.

In some cases, the gap can be even larger.

Think about that for a moment.

Two drivers.

Same vehicle.

Same neighborhood.

Same driving record.

Completely different premiums.

All because of credit history.

Not Every State Allows This Practice

This part often surprises people.

Insurance rules vary dramatically depending on where you live.

Several states, including California, Hawaii, Massachusetts, and Michigan, restrict or prohibit insurers from using credit information when setting premiums.

That means your location matters.

A lot.

The exact same driver could receive very different quotes simply because they moved across state lines.

That’s why national averages rarely tell the whole story.

Why This Matters More In 2026

Insurance costs have been rising across the country.

Repair costs continue increasing.

Modern vehicles contain expensive sensors and technology.

Medical costs remain high.

Severe weather events create additional claims.

All of those factors affect premiums.

When rates rise across the board, the penalty associated with poor credit becomes even more noticeable.

A small percentage increase on an already expensive premium quickly becomes painful.

Also Read:

https://driveglobalnews.in/how-much-does-luxury-car-insurance-cost-in-2026/ – Why insurance costs can surprise luxury vehicle owners.

The Insurance Shopping Mistake Most Drivers Make

Many people stay with the same insurance company for years.

Sometimes decades.

There’s nothing wrong with loyalty.

But insurance companies don’t always reward it.

Drivers with poor credit often benefit significantly from comparing quotes.

Different insurers weigh risk differently.

One company might view your profile favorably.

Another might not.

The difference can be substantial.

That’s why shopping around matters.

Especially after major life changes.

What Can You Actually Do About It?

The obvious answer is improving your credit score.

Easier said than done.

But even small improvements can help over time.

Pay bills consistently.

Reduce outstanding balances.

Review your credit reports for errors.

Avoid unnecessary debt.

Meanwhile, there are other ways to reduce premiums.

Increase your deductible.

Bundle policies.

Ask about discounts.

Maintain a clean driving record.

Take defensive driving courses if available.

Every little bit helps.

The Vehicle You Drive Matters Too

Some vehicles cost more to insure regardless of credit.

High-performance cars.

Luxury vehicles.

Popular theft targets.

Expensive EVs.

If you’re already dealing with higher premiums because of credit, choosing an affordable, reliable vehicle becomes even more important.

Insurance isn’t just about the driver.

It’s about the entire risk profile.

Also Read:

https://driveglobalnews.in/10-vehicles-with-the-lowest-ownership-costs-in-america/ – Vehicles that help keep insurance and ownership costs manageable.

The Bigger Question

Whether insurers should use credit information remains controversial.

And that’s understandable.

Many drivers believe insurance should focus exclusively on driving behavior.

Not financial history.

Others argue that insurance pricing should rely on any data that improves risk assessment.

The debate isn’t ending anytime soon.

But while lawmakers and insurers continue discussing the issue, drivers still need to navigate the current system.

The Quote That Changes Everything

Many people don’t discover the impact of their credit score until they’re shopping for a new policy.

The quote arrives.

The number feels surprisingly high.

And suddenly, something that seemed unrelated to driving becomes very relevant.

That’s frustrating.

But it also creates an opportunity.

Because once you understand how insurance companies calculate risk, you can start making smarter decisions.

Not overnight.

But gradually.

And over time, those decisions can save real money.

Because in 2026, your driving record still matters.

Your vehicle still matters.

Your location still matters.

But for millions of Americans, one number sitting quietly in the background matters more than they ever expected.

Their credit score.