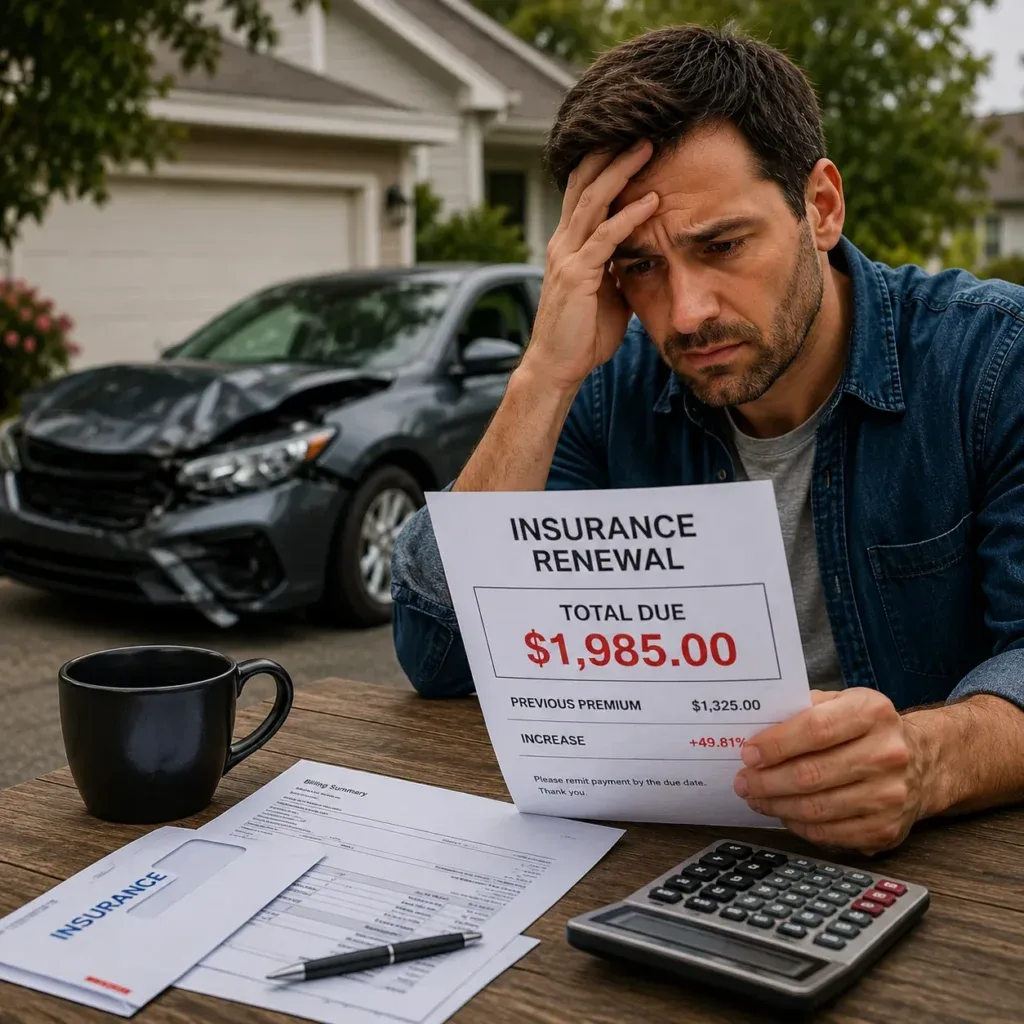

I still remember the sick feeling in my stomach when I opened my insurance renewal letter last month — my premium had jumped almost 40% after a minor fender bender. Unfortunately, I’m not alone. Across America, drivers are seeing car insurance rates after an accident skyrocket in 2026, with average increases hitting 43%.

If you’ve recently been in an accident, you’re probably staring at a big bill too. Here’s what’s really going on and — more importantly — what you can actually do about it.

Why Insurance Rates Are Surging After Accidents in 2026

Insurance companies are losing money. Repair costs for modern vehicles have gone through the roof because of expensive sensors, cameras, and aluminum body panels. Add in inflation, more distracted driving claims, and higher medical costs, and insurers are raising rates aggressively to stay profitable.

A single at-fault accident can now stay on your record for 3-5 years, and in 2026 the penalty is heavier than ever. Even accidents that seemed minor are triggering big hikes.

How Much Can Your Rates Actually Go Up?

The 43% average increase is real, but it varies widely. Some drivers see 20-30% jumps, while others with multiple claims or poor credit are facing 50-70% increases. In high-risk states or big cities, the numbers can be even worse.

Smart Ways to Fight Back and Lower Your Premium

Don’t just accept the higher rate. Here are practical steps that actually work in 2026:

- Shop Around Immediately Don’t renew with the same company without checking competitors. Many drivers save 15-35% just by switching after an accident. Use online comparison tools and talk to independent agents.

- Ask for Forgiveness Programs Some insurers offer “accident forgiveness” if you’ve been a long-term customer with a clean record before the incident. It’s worth calling and asking nicely.

- Improve Your Driving Score Many companies now use telematics (apps that track your driving). Safe driving for 6-12 months can bring your rates down significantly.

- Raise Your Deductible If you can afford to pay more out-of-pocket, increasing your deductible can lower monthly premiums substantially.

- Bundle and Review Discounts Combine home + auto, add anti-theft devices, or take defensive driving courses. These discounts are still valuable in 2026.

- Consider Usage-Based Insurance If you don’t drive much, pay-per-mile policies can save hundreds per year.

When to Consider Keeping the Same Company

Sometimes staying put makes sense — especially if you have multiple policies or your accident was not at fault. Loyalty can occasionally get you better renewal offers.

The One Thing You Must Do Right Now

Don’t wait for your renewal notice. Start comparing quotes 60-90 days before your policy ends. The insurance market is changing fast in 2026, and the best deals go to people who act early.

Final Thoughts

Getting hit with a big insurance rate increase after an accident feels unfair, especially when 43% feels like punishment on top of the stress you already went through. But you don’t have to accept it lying down.

Many drivers successfully fight back and bring their rates down. It takes some effort, but it’s worth it when you see the savings.

If you’re dealing with higher premiums right now, you’re not alone — and there are real ways to improve the situation. Have you managed to lower your rates after an accident? Share your experience in the comments below. I read every single one.

In the meantime, if you’re also looking at new or used vehicles, check our guide on the most American-made cars you can buy in 2026 — it might help you make a smarter long-term choice.