Insurify just published its June 2026 car insurance report — and the headline number is one that most American drivers will find either reassuring or infuriating depending on where they live.

The national average for full coverage car insurance held steady at $186 per month through May. Liability-only coverage: $98 per month.

That’s the good news. Rates have been declining throughout 2026 after the brutal 46% increase between 2022 and 2024. The bad news? “Declining nationally” is doing a lot of work in that sentence. Because if you live in Maryland, Rhode Island, or Nevada — your rates are nowhere near $186 per month. And if you live in New Hampshire — you’re paying less than half that.

Here’s the full picture.

The Most Expensive States Right Now

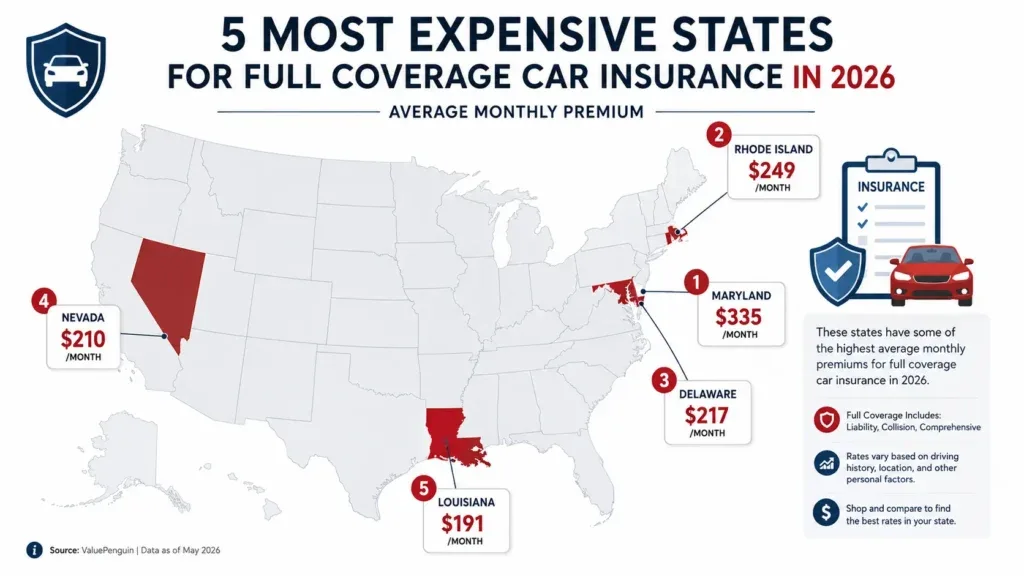

Maryland — Most Expensive in America

Maryland knocked Washington D.C. off the top spot for the most expensive car insurance in the country. If you’re driving in Maryland right now, you’re paying significantly above the national average. Dense traffic, high repair costs, and an accident rate that keeps insurers pricing cautiously are the main drivers.

Rhode Island — Permanently in the Top Five

Rhode Island has been in the top five most expensive states for car insurance for years. Small state, dense population, high litigation costs after accidents. The formula hasn’t changed, and neither have the rates.

Delaware — Newly Back in Top Five

Delaware returns to the top five this month, replacing New York. Delaware’s rates have been climbing as the state’s insurance market adjusts to rising claims costs — particularly around medical payments after accidents. State legislators actually introduced a reform task force in mid-2025 specifically to address the escalating costs. Results are slow.

Nevada — $335 per month

Las Vegas accident rates, extreme heat that accelerates vehicle wear, and a high density of uninsured drivers combine into rates that are over 50% above the national average. If you’re moving to Nevada, budget accordingly.

Louisiana — $327 per month

High uninsured driver rates, frequent severe weather claims, and a legal environment historically favorable to large personal injury verdicts. Louisiana has been consistently among the most expensive states for decades. That’s not changing soon.

The Cheapest States Right Now

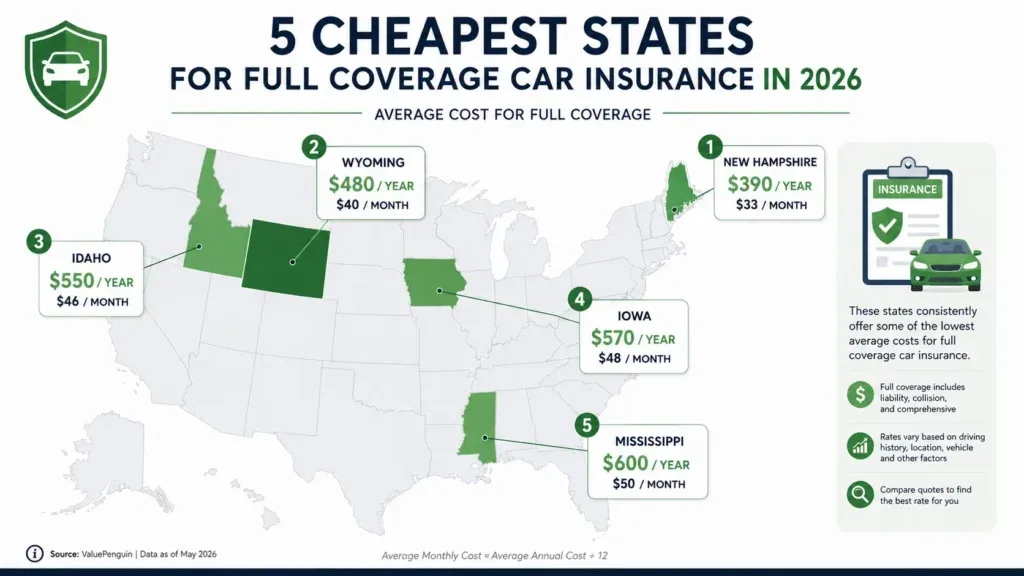

New Hampshire — $957 per year ($80 per month)

New Hampshire keeps the title of most affordable car insurance in America. Under $80 per month for full coverage. The combination of low population density, no minimum coverage requirement (though most drivers buy it anyway), and a claims environment that insurers find manageable keeps New Hampshire rates remarkably low.

Wyoming — $1,052 per year

Wyoming had one of the biggest rate drops of any state in 2025 — down over 30% — and remains one of the cheapest in 2026. Open roads, low traffic density, minimal litigation. Insurers like writing policies in Wyoming.

Iowa — Biggest Decrease in 2026

Iowa has the largest estimated rate decrease of any state in 2026 — down 6.19%. Combined with rates that were already below average, Iowa drivers are getting the clearest benefit of the insurance market correction that’s been underway since 2025.

Idaho — $1,244 per year

Idaho consistently ranks in the five cheapest states. Low crime rates, manageable weather exposure compared to tornado and hurricane states, and driving demographics that generate fewer severe claims.

The Most Expensive Car to Insure Right Now

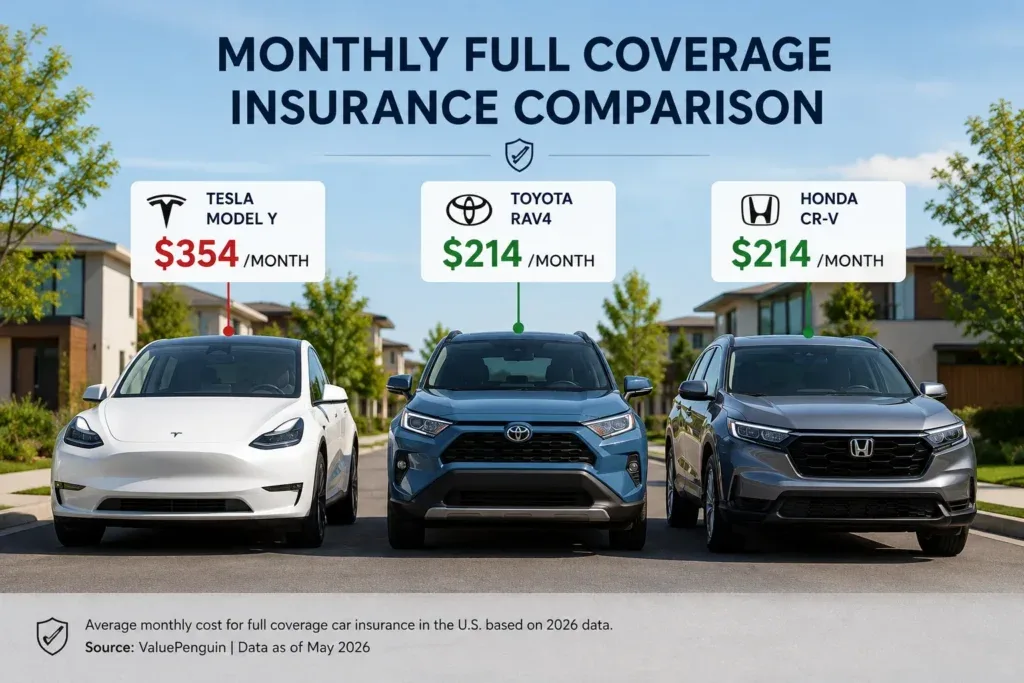

This number will surprise people who bought a Tesla thinking they were making a financially savvy decision.

The Tesla Model Y is the most expensive new car to insure in America in 2026, at an average of $354 per month for full coverage — according to ValuePenguin’s analysis of the most popular 2025-2026 models.

That’s $4,248 per year. Just for insurance. On a car that starts at $44,990.

For comparison: the Toyota RAV4 and Honda CR-V are the most affordable popular new cars to insure, at approximately $214 per month — 40% less than the Tesla.

The reason EVs from Tesla and Rivian cost significantly more to insure than EVs from legacy manufacturers is specific and data-driven. Replacement parts from Tesla are expensive and sometimes slow to source. Repair costs per claim are higher. And Tesla’s vehicles attract a statistical profile of driver that generates more severe claims. In contrast, a Hyundai Ioniq 5 or Chevrolet Equinox EV — built by legacy manufacturers with widely available parts and established repair networks — costs approximately 49% less to insure than a comparable Tesla.

If you’re considering a Tesla specifically as a cost-saving measure — factor the insurance premium into your math before you sign.

What Changed Between 2025 and Now

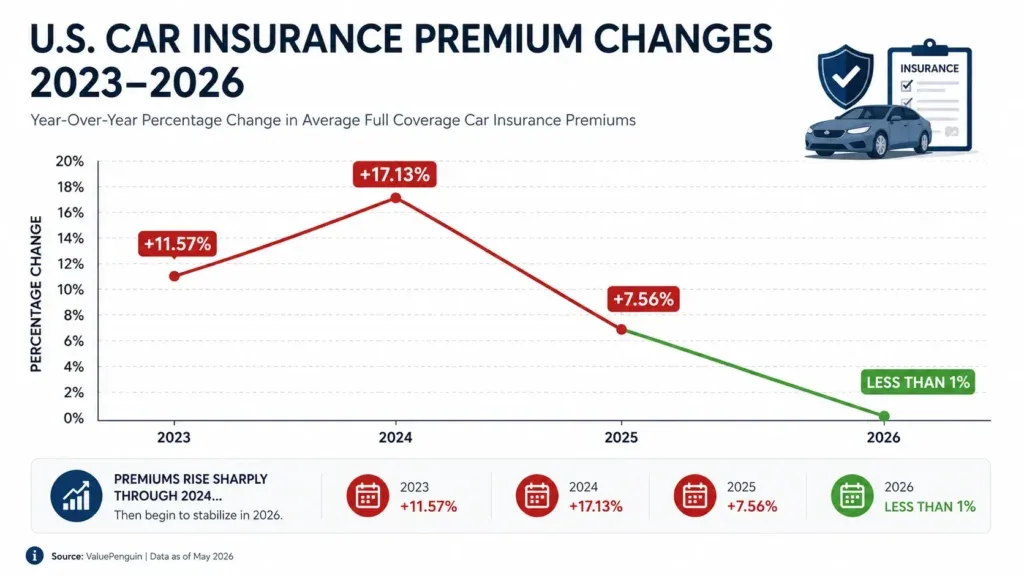

After three years of brutal premium increases — 11.57% in 2023, 17.13% in 2024, and 7.56% in 2025 — 2026 finally brought relief for most American drivers. Rates fell 6% nationally in 2025, and 2026 is projecting less than 1% increase nationally.

Why? Insurance companies spent 2023-2025 aggressively repricing to recover margins after a period where rising repair costs, increased accident severity, and more frequent weather claims made their existing pricing unprofitable. By the end of 2025, most major insurers had rebuilt their financial cushion. They’re now competing for new customers again — which means more competitive pricing rather than panic-driven increases.

State Farm cutting rates 4% in 2026. Multiple other large carriers holding flat or reducing modestly. The market is genuinely more favorable than it’s been in three years.

The wildcard that could change this trajectory: tariffs on imported auto parts. The 25% EU tariffs and Korean tariff uncertainty from earlier this year haven’t fully worked through to repair costs yet. When a replacement bumper costs 20% more because of tariff-driven parts price increases, insurers eventually pass that cost to policyholders. That pricing adjustment is expected to begin appearing in late 2026 renewals — particularly for owners of European and Korean vehicles.

What You Should Do Before Your Next Renewal

Insurify’s data comes from 97 million real quotes across 50+ partner insurance companies. Their consistent finding: the average driver can save $700-$1,100 per year simply by shopping at renewal rather than automatically renewing.

The current market — with multiple large carriers in competitive mode — is particularly favorable for shopping. State Farm cutting 4% means a driver who moves from Allstate (raising 1.98%) to State Farm captures nearly a 6% swing before any other factors.

Three specific actions worth taking this month:

Check whether your state is in the declining or increasing group. Iowa, Minnesota, and Nebraska are seeing decreases. Maryland, Rhode Island, and Nevada are not. If you’re in a declining state, your renewal quote should reflect that. If it doesn’t — your insurer is keeping the savings rather than passing them to you.

Get at least three quotes. Insurify, The Zebra, or direct quotes from Travelers, GEICO, Progressive, and State Farm. It takes 20 minutes. The potential savings are real.

Ask your current insurer specifically about rate reductions. Some insurers apply rate decreases automatically at renewal. Others wait to be asked. A single phone call — “I’ve seen that State Farm is cutting rates 4% in 2026. What’s happening with my rate at renewal?” — can produce results without switching.

The insurance market is the most favorable it’s been since 2022. The drivers who benefit are the ones who actually go looking for the savings.