How to Save $1,200 on Car Insurance in 2026 : Most people treat car insurance the same way they treat their internet bill.

They set it up once.

Pay it every month.

And assume the price is the price.

That’s exactly what insurance companies hope you’ll do.

Because loyalty doesn’t always save money.

In fact, it often costs money.

A lot of it.

With insurance premiums climbing across America in 2026, many drivers are paying hundreds—or even thousands—more than necessary.

The good news?

Reducing your premium doesn’t require a perfect driving record or endless phone calls.

Small changes can create surprisingly large savings.

Here are six moves that actually work.

1. Shop Around Before Your Renewal Date

This sounds obvious.

Most people still don’t do it.

Insurance companies constantly adjust pricing models.

The company that offered the best rate last year may not offer the best rate today.

Get quotes from at least three insurers before your policy renews.

The process takes less time than most people expect.

And the savings can be dramatic.

Many drivers save several hundred dollars simply by switching companies.

Also Read:

https://driveglobalnews.in/best-car-insurance-companies-for-suv-owners-2026/ – The insurers offering competitive rates for family SUVs.

2. Bundle Your Policies

If you have homeowners, renters, or life insurance, ask about bundling.

Many insurers reward customers who purchase multiple products.

The discounts vary.

But savings of 10% to 25% are common.

More importantly, managing fewer policies can simplify your financial life.

That’s a win beyond the monthly premium.

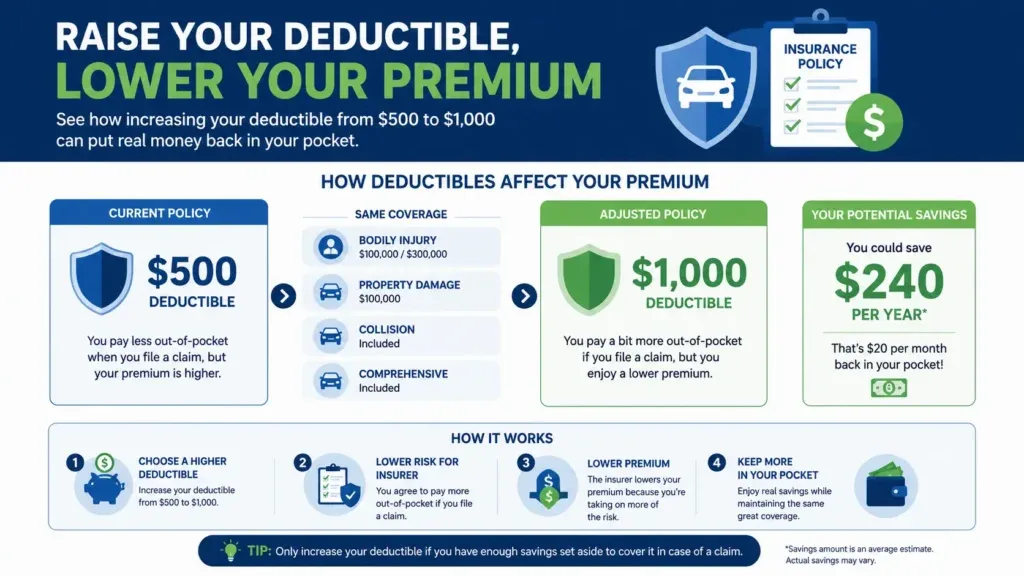

3. Increase Your Deductible

A higher deductible usually means a lower premium.

Moving from a $500 deductible to a $1,000 deductible can reduce your annual insurance costs.

Just be realistic.

Choose a deductible you could comfortably afford if an accident happened tomorrow.

The goal isn’t to create financial stress.

It’s to avoid paying extra every month for coverage you may never use.

4. Review Coverage You No Longer Need

Many drivers continue paying for coverage that no longer makes sense.

Own an older vehicle?

Comprehensive and collision coverage may not be worth the cost.

Drive fewer miles than you used to?

A low-mileage program could lower your rate.

Life changes.

Insurance should change with it.

Review your policy annually.

Not because you’re looking for mistakes.

Because your needs evolve.

5. Take Advantage of Telematics Programs

Many insurers now offer usage-based insurance programs.

These programs track driving habits through a mobile app or plug-in device.

Safe drivers often receive meaningful discounts.

The biggest savings usually go to drivers who:

- Avoid hard braking

- Drive fewer miles

- Avoid late-night driving

- Maintain consistent speeds

These programs aren’t for everyone.

But if you’re a careful driver, they can make a real difference.

6. Improve Your Credit Score

This surprises many people.

In most states, insurers consider credit-based insurance scores when calculating premiums.

Better credit can lead to lower rates.

Improving your credit won’t reduce your premium overnight.

But over time, it can help.

Pay bills on time.

Reduce outstanding balances.

Review your credit reports regularly.

Small improvements matter.

Also Read:

https://driveglobalnews.in/does-your-credit-score-affect-car-insurance-2026/ – The honest truth about how credit influences insurance premiums.

The Biggest Mistake Drivers Make

They focus only on the monthly payment.

That’s understandable.

But the monthly number can hide expensive decisions.

A lower payment with inadequate coverage isn’t a bargain.

It’s a risk.

Saving money matters.

Protecting yourself matters more.

Always compare coverage levels before choosing the cheapest quote.

How Much Can You Actually Save?

Not every driver will save $1,200.

Some will save less.

Some will save more.

The key is stacking multiple strategies together.

Switch insurers.

Bundle policies.

Adjust your deductible.

Review your coverage.

Improve your credit.

Each step creates incremental savings.

Combined, they can dramatically reduce your costs.

The Best Time to Lower Your Insurance Bill

Most people wait until their renewal notice arrives.

That’s too late.

The best time to review your insurance is before you need to.

Before rates increase.

Before your circumstances change.

Before you assume you’re getting a fair deal.

Because insurance companies review your profile regularly.

You should do the same.

Five minutes of research once a year can save hundreds of dollars.

And unlike many financial goals, this one doesn’t require earning more money.

It simply requires paying closer attention to where your money is already going.

Because the easiest way to improve your budget isn’t always finding extra income.

Sometimes it’s stopping unnecessary expenses from quietly renewing every six months.