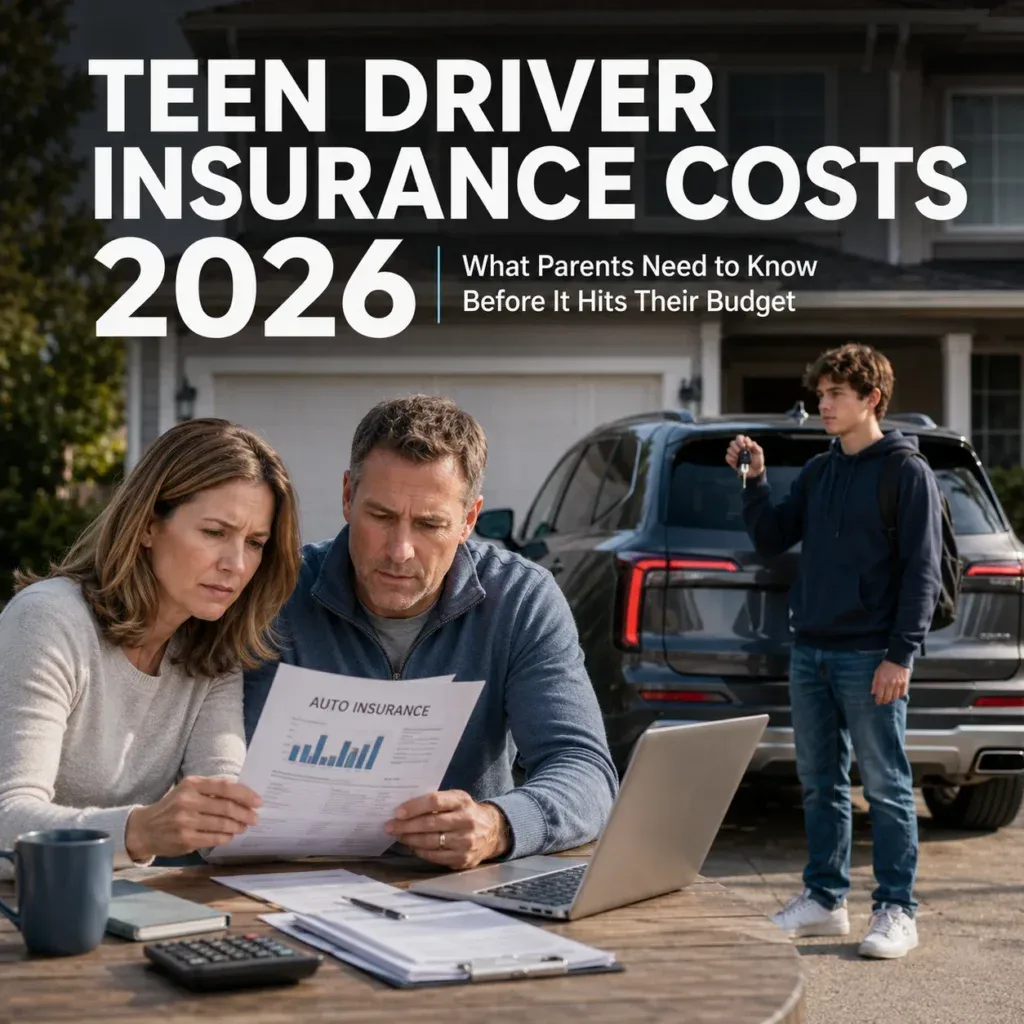

What Happens to Your Car Insurance : There’s a moment almost every parent remembers.

You’re sitting in the passenger seat.

Your teenager is behind the wheel.

Both hands are gripping the steering wheel tightly.

You’re trying to look calm.

They’re trying to look confident.

And somewhere between the first stop sign and the first highway merge, a new thought enters your mind.

“How much is this going to cost me?”

Not the driving lessons.

Not the extra gas.

The insurance.

Because adding a teen driver to your policy is one of the biggest changes most families ever make to their car insurance.

And in 2026, the numbers can be surprising.

Very surprising.

Why Teen Drivers Cost More to Insure

Insurance companies price policies based on risk.

Teen drivers represent a lot of it.

New drivers have less experience.

They’re more likely to be involved in accidents.

They’re more likely to file claims.

And they’re more likely to underestimate dangerous situations.

That’s not criticism.

It’s simply reality.

Every experienced driver was once a nervous beginner.

Insurance companies know this.

And premiums reflect it.

How Much Will Your Premium Increase?

This is the question every parent asks.

The answer depends on several factors.

Your location.

Your insurance company.

Your vehicle.

Your teen’s age.

Their driving history.

But here’s the important part.

Most families should expect their insurance premium to increase significantly.

In many cases, adding a teen driver can raise annual premiums by 50% to 150% or more.

For some households, that could mean an additional $1,500 to $4,000 per year.

Sometimes even higher.

The exact number varies.

The sticker shock doesn’t.

The Vehicle Matters More Than You Think

A teenager driving a high-performance sports car is expensive to insure.

A teenager driving a safe, reliable family sedan is much less expensive.

Insurance companies pay close attention to the vehicle.

Safety ratings matter.

Repair costs matter.

Horsepower matters.

The vehicle you assign to your teen can dramatically affect your premium.

That’s why many families choose practical vehicles with strong safety reputations.

Also Read:

https://driveglobalnews.in/5-cars-with-the-cheapest-insurance-for-families-in-2026/ – Family-friendly vehicles that help keep insurance costs manageable.

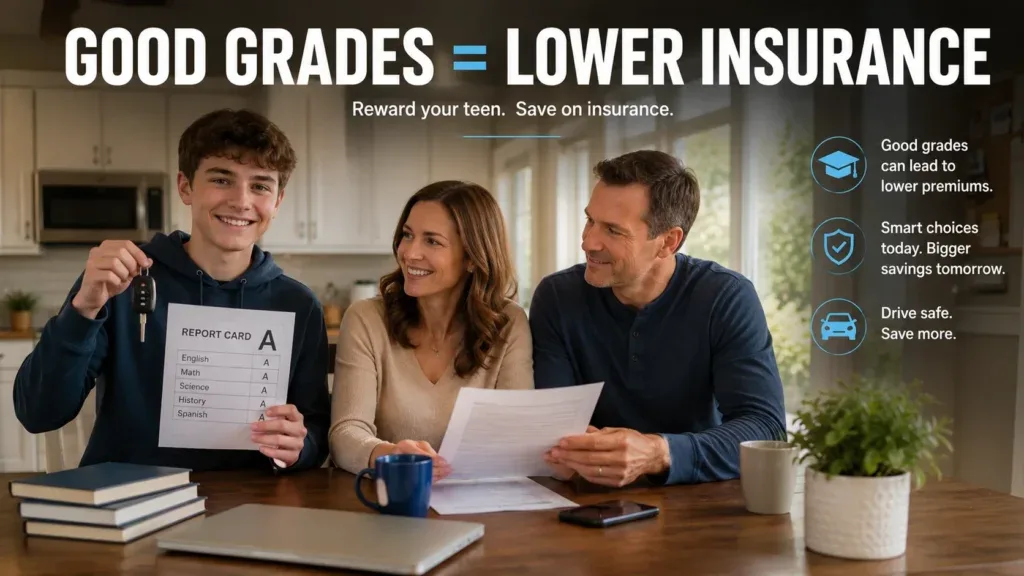

Good Grades Can Save Real Money

Many insurers offer good student discounts.

The reasoning is simple.

Students who perform well academically often file fewer claims.

Requirements vary by company.

But maintaining a strong GPA could reduce insurance costs.

It’s one of the easiest ways for families to save money.

And unlike many discounts, it rewards something parents already encourage.

Driver Education Still Matters

Completing an approved driver’s education course can also help lower premiums.

These courses don’t eliminate the risk associated with new drivers.

But they can demonstrate a commitment to safer driving habits.

Insurance companies appreciate that.

The savings may not be dramatic.

But every discount helps.

Especially when premiums increase as much as they often do.

Should Your Teen Have Their Own Policy?

Usually, no.

Adding a teen driver to a family policy is often significantly cheaper than purchasing a separate policy.

There are exceptions.

But for most families, keeping everyone under the same policy makes financial sense.

The key is comparing options.

Never assume.

Always ask your insurer to run multiple scenarios.

The difference can be substantial.

The Biggest Mistake Parents Make

Many families wait until the last minute to call their insurance company.

That’s a mistake.

Request quotes before your teenager gets a license.

Understand the financial impact early.

Explore discounts.

Review coverage options.

Planning ahead gives you time to make smart decisions.

Waiting creates expensive surprises.

Also Read:

https://driveglobalnews.in/car-insurance-for-bad-credit-2026-how-much-more-are-you-paying/ – Why factors beyond driving history can dramatically affect insurance rates.

This Isn’t Just About Money

It’s about responsibility.

Adding a teen driver creates an opportunity to discuss safe driving habits.

Distracted driving.

Speeding.

Phone use.

Insurance costs become more meaningful when teenagers understand how their decisions affect the family budget.

Accidents don’t just impact premiums.

They affect trust.

Confidence.

And safety.

Those conversations matter.

The First Solo Drive

Eventually, the day arrives.

Your teenager grabs the keys.

Walks to the car.

And drives away alone for the first time.

You’ll probably stand in the driveway longer than necessary.

Not because you’re worried about the insurance bill.

Because you’re realizing something bigger.

Teaching someone to drive isn’t just about transportation.

It’s about independence.

Responsibility.

Growing up.

The insurance premium is part of that journey.

An expensive part, admittedly.

But temporary.

The lessons your teenager learns behind the wheel will last much longer.

And in the end, that’s what matters most.