Memorial Day weekend. 39.1 million Americans on the road. Hundreds of miles driven. And somewhere in all of that driving — a detail that most people don’t know costs them money every single year.

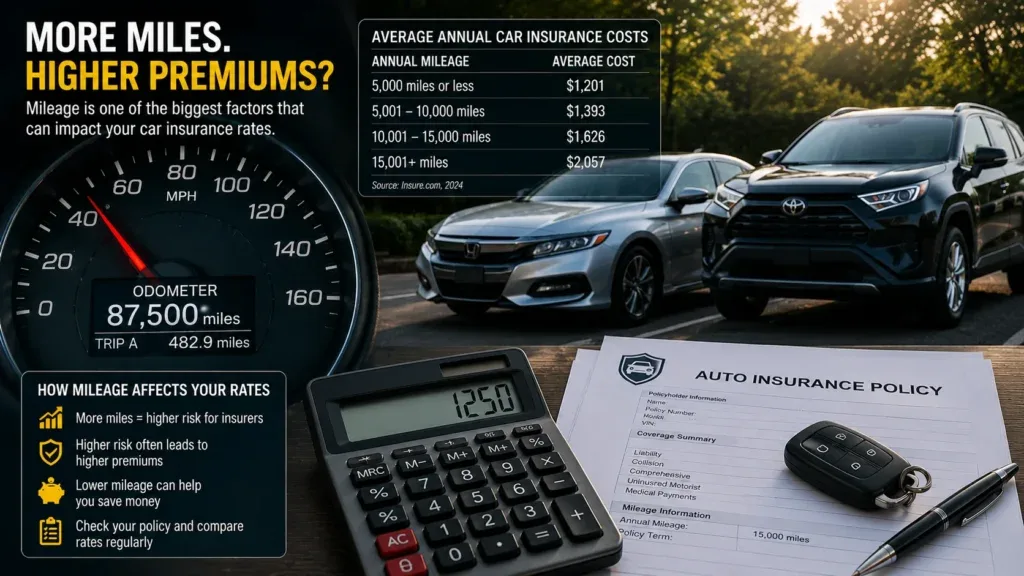

How much you drive directly affects what you pay for car insurance.

Not slightly. Not theoretically. The difference between a low-mileage driver and a high-mileage driver can be $300-$600 per year on the same car, with the same driving record, at the same insurer. Here’s exactly how it works.

also read : https://driveglobalnews.in/how-much-does-car-insurance-cost-for-a-new-driv/

The Mileage Tiers That Actually Matter

Insurance companies categorize annual mileage into buckets. The exact thresholds vary by insurer, but the general framework most companies use looks like this:

Under 7,500 miles per year — Low mileage This is where insurers start offering meaningful discounts. Drivers in this tier are statistically less exposed to accidents simply because they spend less time on the road. Less time driving = fewer opportunities for something to go wrong.

7,500 to 15,000 miles — Standard/Average The national average is roughly 13,500 miles per year. Most standard rate quotes are built around this range. If you’re in this band, you’re paying the baseline rate.

15,000 to 25,000 miles — Above average Rates begin to increase at this level. Some insurers apply a surcharge of 5-15% for drivers in this range compared to the average mileage baseline.

Over 25,000 miles — High mileage This is where the premium impact becomes significant. Drivers covering 25,000+ miles annually are statistically much more likely to be involved in an accident simply due to exposure time. Rate increases of 15-25% over the standard rate are common at this level.

A driver covering 30,000 miles per year — which isn’t unusual for outside sales, real estate agents, or long-distance commuters — might pay $400-$700 more per year than an identical driver covering 10,000 miles. Same car. Same record. Same location. Just more miles.

What Actually Happens When You Lie About Mileage

This comes up every time mileage and insurance are discussed. The honest answer is worth knowing.

When you apply for auto insurance, you’re asked to estimate your annual mileage. Most people underestimate — sometimes accidentally, sometimes intentionally, because lower mileage estimates often produce lower quotes.

In states that allow credit-based insurance scoring and telematics data, insurers are increasingly able to verify mileage through connected car data, odometer readings at claims time, and renewal checks. If you report 8,000 miles annually and then make a claim with 22,000 miles on the odometer — the discrepancy will be noted.

The consequence ranges by insurer and state. Some simply recalculate your premium retroactively and bill the difference. Others can deny a claim on the grounds of material misrepresentation — meaning your policy wasn’t valid because you provided inaccurate information. The risk of a denied claim on a major accident far outweighs any premium savings from underreporting mileage.

Report honestly. The premium difference isn’t worth the risk.

also read : https://driveglobalnews.in/cheapest-car-insurance-companies-in-2026/

The Low-Mileage Discounts That Actually Work

If you genuinely drive less than average — you should be paying less and most people aren’t claiming the savings available to them.

Metromile and Mile Auto — pay-per-mile insurance For drivers covering fewer than 7,500 miles annually, pay-per-mile insurance models can deliver dramatic savings. Metromile’s structure: a flat base rate of approximately $29-$49 per month plus 3-6 cents per mile driven. A driver covering 5,000 miles annually with a $40 base rate and $0.05 per mile pays approximately $730 per year — potentially $1,000+ less than a standard policy for the same coverage.

State Farm Drive Safe & Save State Farm’s telematics program gives low-mileage drivers discounts of up to 30%. The program tracks both mileage and driving behavior — smooth acceleration, minimal hard braking, and lower annual miles all contribute to the discount. If you work from home, drive rarely, or live where public transit covers most of your trips — this program can make State Farm the cheapest option for your profile.

Progressive Snapshot Similar to Drive Safe & Save, Snapshot monitors your driving and rewards low mileage plus safe driving with discounts up to 30%. Progressive’s telematics program is the largest in the industry by enrollment and has been running long enough that the discount structure is well-calibrated and reliable.

Road Trips and Your Insurance — What Changes

Memorial Day weekend raises a specific question: does a long road trip affect your insurance rate?

The short answer: no, a single road trip doesn’t trigger a rate change. Your insurer doesn’t know you drove 1,200 miles this weekend versus your typical 50-mile week. Rate calculations happen at renewal based on annual mileage estimates and claims history — not individual trip data.

However: if you’re enrolled in a telematics program and your weekend driving adds significant miles that push you into a higher annual mileage tier, that data does factor into your renewal discount calculation. If you’re on pay-per-mile insurance — you’re paying per mile including road trips. A 600-mile Memorial Day round trip on Metromile at $0.05 per mile costs $30 in mileage fees. For a driver who rarely travels that’s still likely cheaper than annual standard insurance, but it’s worth knowing before you commit to the model.

The Practical Takeaways

If you drive under 10,000 miles annually — call your insurer today and make sure your policy reflects that accurately. Most people set their mileage estimate at application and never update it. If you’ve started working from home, moved closer to work, or simply drive less than you used to — a corrected mileage estimate at renewal could lower your premium $150-$400 per year.

If you drive over 20,000 miles annually — shop your insurance aggressively at each renewal. Companies price high-mileage drivers differently, and the variation between carriers for high-mileage profiles is larger than for average drivers. Travelers, Progressive, and USAA (if eligible) consistently offer the most competitive rates for high-mileage drivers among major carriers.

If you’re undecided on pay-per-mile insurance — do the math on your actual miles before committing. It’s the right product for genuinely low-mileage drivers and the wrong product for anyone who takes multiple road trips or covers more than 10,000 miles annually.

Memorial Day weekend is a great time to be on the road. It’s also a surprisingly good time to think about whether your insurance actually reflects how you drive.