Tuesday May 12, 2026 delivered an economic data point that every American household felt before they ever saw the number.

The Consumer Price Index rose 3.8% year-over-year in April 2026 — the highest inflation reading since 2023. Gas prices jumped 28.4% over the last year. The national average hit $4.50 per gallon as of Tuesday.

And then the number that really stings: after adjusting for inflation, real wages fell for the first time in three years.

For car buyers, this data isn’t abstract. It changes the math on every vehicle purchase decision being made right now.

Why Gas Is the Story Inside the Story

Every inflation story this month points back to the same source: Iran’s blockade of the Strait of Hormuz, which began when the US entered the conflict on February 28. About 20% of global oil supply moves through that strait. When it gets blocked, the consequences flow through every energy-dependent price in the economy.

Gas up 28.4%. Airfare up 20.7%. Grocery prices up 3.2%. Beef up 14.8%.

Economists are not optimistic about a fast resolution. The most pessimistic scenario, according to Oxford Economics, is six to nine months before supply chains normalize — even if the conflict ends relatively soon. “The trajectory of inflation will not immediately reverse, even if geopolitical tensions ease,” said one economist. Translation: $4.50 gas is not a temporary blip you can wait out.

And because real wages fell — meaning paychecks are growing slower than prices — American consumers are actually worse off financially today than they were a year ago. That has direct implications for car buying.

What Falling Real Wages Mean for Car Buyers

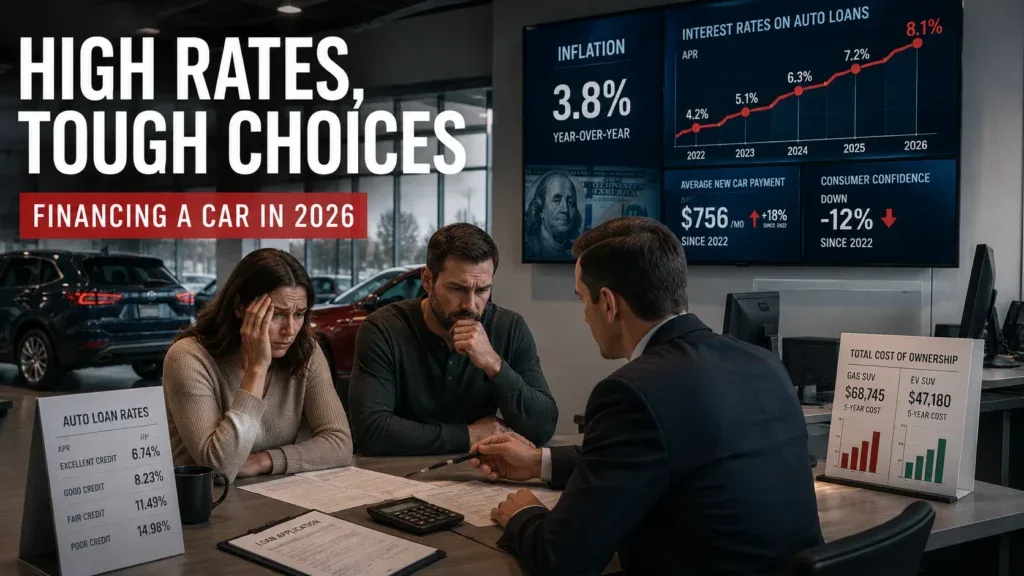

Here’s the uncomfortable reality: the average new car payment is already $812 per month. That’s before the inflation data from Tuesday. With real wages now falling and everyday costs climbing — food, gas, airfare — the monthly budget available for a car payment has effectively shrunk for most American households.

This creates two different car buying situations right now:

Buyers who must buy a vehicle — because of a breakdown, a growing family, or a job requirement — face a market where prices are high, rates haven’t fallen (the Fed signaled no rate cuts this year given the inflation trajectory), and every dollar of the car payment competes with $4.50 gas and $14.8%-higher grocery bills.

For these buyers, the calculus is simple and urgent: choose the vehicle whose total monthly cost of ownership is lowest, not the one with the most compelling sticker price. A $35,000 EV charging at home for 4 cents a mile is a fundamentally different monthly budget than a $30,000 gas SUV costing 16 cents a mile at current prices.

Buyers who can delay face a more nuanced question: does waiting actually help? The economists say no. Gas prices are unlikely to fall quickly. Interest rates are unlikely to fall this year. New car inventory tightness on popular hybrids isn’t improving fast. Waiting in this environment means paying the same high gas prices in your current vehicle while the window for current-model-year pricing closes.

also read : https://driveglobalnews.in/rivian-r2-vs-bmw-ix3-in-2026-two-of-the-year/

The EV and Hybrid Math Has Never Been Clearer

Here’s the number that every car shopper needs to see right now.

At $4.50 per gallon with a gas car averaging 28 MPG: $0.16 per mile in fuel costs.

Charging a Hyundai Ioniq 5 at home on a Level 2 charger: approximately $0.04 per mile.

The difference: $0.12 per mile. At 13,500 annual miles — $1,620 per year in fuel savings for an EV owner versus a comparable gas car owner.

For a hybrid like the Toyota RAV4 at 40 MPG: $0.113 per mile in fuel costs — saving roughly $630 per year versus the average gas car at current prices.

These numbers have always existed in favor of electrified vehicles. At $4.50 gas, they’re no longer a financial planning exercise. They’re a monthly budget difference that most families will feel immediately.

The Rate Cut That’s Not Coming

One piece of news that came alongside the inflation data is worth noting for buyers planning to finance a vehicle: the Federal Reserve signaled strongly on Tuesday that no interest rate cuts are expected in 2026 given the inflation trajectory.

Car loan rates have been elevated since 2023. Most buyers are financing at 6.5-8% depending on credit score and lender. With no Fed cuts coming, those rates aren’t moving down this year.

The practical advice: if your credit score is 750+, shop rates aggressively before visiting any dealership. Credit unions often beat bank rates by 1-2 percentage points — which on a $35,000 loan over 60 months is roughly $1,400 in total interest savings. On a $50,000 loan over 72 months, it’s over $2,800.

In an inflationary environment where real wages are falling, every dollar of loan interest savings matters.

also read : https://driveglobalnews.in/alfa-romeos-electric-giulia-is-coming-in-2026/

The Bottom Line for May 2026

The inflation data released Tuesday makes the financial case for hybrids and EVs stronger than it has been at any point in the modern era of electrified vehicles. $4.50 gas, falling real wages, and no rate cuts in sight create an environment where the running cost of a gas vehicle is genuinely painful for middle-class American households.

The vehicles that insulate buyers from that pain — the Tucson Hybrid, the RAV4 Hybrid, the Ioniq 5, the Sportage Hybrid — are the ones where the monthly total cost of ownership argument is now overwhelming.

Buy the car that costs you less to own every month. In May 2026, that math points in one direction clearly.